SME Finance Guide 2025: Business Lending & Funding Options

Running a small or medium-sized enterprise (SME) is exciting, but one challenge most business owners face is securing the right capital at the right time. Whether you’re looking to expand operations, purchase new equipment, or manage day-to-day cash flow, understanding the SME finance landscape in 2025 is critical. This guide will break down key business lending options, government programs, and alternative funding sources to help SMEs make informed decisions.

The State of SME Finance in 2025

The business loan market has seen considerable evolution in recent years. Traditional banks remain a primary source of funding, but 2025 is witnessing a significant shift toward fintech and alternative lenders. While interest rates have fluctuated globally, access to finance remains challenging for some SMEs, particularly those without a strong credit history or collateral.

Despite these challenges, opportunities abound. Digital lenders now offer faster approvals and flexible repayment terms, while government-backed programs provide safety nets and incentives for small businesses. Knowing what’s available and how it fits your business model is key to long-term growth.

Types of SME Funding Options Available in 2025

1. Traditional Bank Loans

Banks continue to dominate the business lending sector. A traditional SME loan usually comes with structured repayment terms and lower interest rates compared to alternative lenders. However, banks are cautious: approval often requires a solid credit history, collateral, and comprehensive business documentation.

Pros: Lower interest rates, reliable lenders, long-term stability.

Cons: Lengthy approval processes, strict eligibility criteria.

For businesses with strong financials, a bank loan can be the most cost-effective way to secure funding.

2. Government Business Loans & Grants

One of the most valuable resources for SMEs in 2025 is government business loans. These programs often come with lower interest rates, longer repayment periods, or partial loan forgiveness. Some grants and incentives are also available for businesses in specific sectors, such as tech, manufacturing, or renewable energy.

As mentioned in the Business.gov.au Grants and Programs report, the Grants Finder is a comprehensive tool for Australian SMEs to discover federal and state funding programs tailored to their needs. It covers a wide range of initiatives, from startup grants to support for innovation and expansion.

Why consider government support?

- Lower borrowing costs than commercial lenders.

- Increased likelihood of approval for businesses with limited credit history.

- Access to special schemes focused on innovation, employment, or sustainability.

However, eligibility requirements can be strict, and the application process may involve detailed documentation and reporting. Still, for many SMEs, government programs are a vital small business finance support tool.

3. Fintech & Online Lenders

The rise of fintech has transformed access to finance for SMEs. Online lenders offer fast approvals, minimal paperwork, and innovative products like short-term working capital loans or peer-to-peer lending.

Benefits of fintech lending include:

- Quick turnaround, often within 24–48 hours.

- Flexible repayment schedules tailored to cash flow.

- Alternative credit assessment models that consider factors beyond traditional credit scores.

While fintech loans can be convenient, the cost of capital may be higher than traditional bank loans. They are ideal for businesses seeking speed and flexibility rather than the lowest interest rate.

4. Invoice Financing & Factoring

Invoice financing allows businesses to unlock cash tied up in unpaid invoices. Instead of waiting 30–90 days for customer payments, SMEs can access immediate funds. Factoring companies purchase invoices at a small discount, providing liquidity to maintain operations.

This method is especially beneficial for SMEs with fluctuating cash flow or seasonal revenue patterns. It also helps in maintaining healthy supplier relationships by ensuring timely payments.

5. Business Lines of Credit & Overdrafts

A business line of credit functions like a revolving loan: you borrow as needed up to a pre-approved limit and pay interest only on the funds used. Similarly, overdrafts give SMEs flexibility to cover short-term cash flow gaps.

These products are ideal for managing daily operations, bridging seasonal income gaps, or handling unexpected expenses without committing to a long-term loan.

6. Equipment & Asset Financing

For SMEs looking to expand operations or upgrade machinery, equipment financing is a practical option. Lenders provide funding specifically for purchasing assets, with the equipment itself often serving as collateral.

Benefits include:

- Preserving cash flow by spreading the cost of expensive assets.

- Potential tax advantages through depreciation.

- Keeping credit lines available for other operational needs.

7. Equity & Venture Capital Funding

For SMEs with high growth potential, raising capital through equity investment or venture capital can be attractive. Investors provide funds in exchange for a share of the business, often bringing strategic guidance alongside capital.

Pros: Large amounts of capital without immediate repayment obligations.

Cons: Loss of some ownership and control, investor expectations for rapid growth.

2025 is seeing increased opportunities in crowdfunding and micro-investing, allowing even smaller businesses to access capital traditionally reserved for larger enterprises.

How to Choose the Right Funding Option

Selecting the right SME funding options depends on several factors:

- Business stage: Early-stage businesses may struggle with bank loans but qualify for government schemes or equity funding.

- Cash flow stability: Reliable cash flow allows safer access to traditional loans or lines of credit.

- Ownership goals: If retaining full control is critical, debt financing may be preferable over equity investment.

- Cost of capital: Compare interest rates, fees, and repayment flexibility.

As stated in the NSW Small Business Grants and Support report, the NSW Rural Assistance Authority provides low-interest loans of up to $130,000 for businesses affected by declared natural disasters. Eligible businesses benefit from a two-year interest-free and repayment-free period, helping them manage cash flow during challenging times.

A simple checklist for SMEs:

- What is the funding needed for?

- How soon do we need access to funds?

- What repayment terms are feasible?

- Are there any tax or accounting implications?

- How will this affect ownership or equity in the business?

Answering these questions can clarify which funding route best suits your growth strategy.

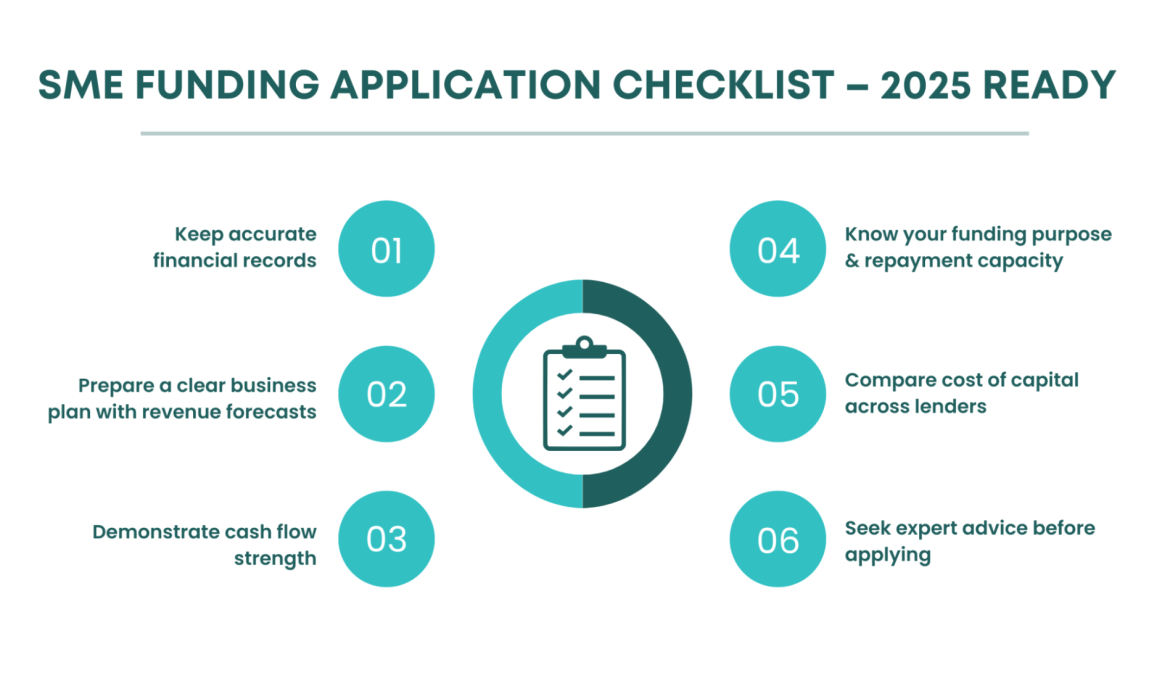

Preparing for a Successful Loan or Funding Application

Regardless of the funding source, preparation is key. Strong documentation and financial planning can significantly improve the chances of approval:

- Maintain accurate books and up-to-date financial statements.

- Prepare a detailed business plan showing revenue projections and growth strategy.

- Demonstrate consistent cash flow and repayment capacity.

- Seek professional advice from accountants or financial advisors to structure the application.

Even in the small business finance support space, lenders appreciate businesses that are proactive and well-prepared.

2025 Lending Trends SMEs Should Watch

Several trends are shaping the business loan market this year:

- Data-driven lending: Lenders increasingly rely on AI and analytics to assess creditworthiness quickly.

- Sustainability-linked finance: Loans tied to ESG goals are becoming more common.

- Alternative credit scoring: SMEs without traditional collateral or credit history can access loans through innovative models.

- Hybrid lending models: A mix of fintech and traditional banking offerings provides more flexibility for SMEs seeking access to finance.

As mentioned in the Queensland Government Small Business Grants report, programs like the Business Basics Grants Program and the Better Local Business Grant Program are designed to support SMEs with funding for operational improvements, technology adoption, and business expansion.

Keeping an eye on these trends helps businesses plan funding strategies effectively.

The Role of Financial Advisors & Outsourced CFO Services

Navigating SME finance can be complex. Professional advisors or outsourced CFOs can:

- Guide SMEs through the various SME funding options.

- Help structure loans or investment deals to reduce cost and risk.

- Monitor cash flow, debt servicing, and repayment schedules.

For businesses serious about growth, leveraging expert financial advice ensures access to the best small business finance support available.

Conclusion

2025 presents SMEs with a diverse array of SME finance options. From traditional SME loans and government business loans to fintech innovations and equity funding, businesses now have more opportunities than ever to secure capital. The key is understanding your business’s needs, planning strategically, and seeking professional support when necessary.

With careful evaluation and the right approach, any SME can access funding, strengthen operations, and fuel growth in a competitive marketplace.

Next Step: Assess your business’s financial health, explore all available SME funding options, and identify which path aligns with your growth vision. Your next funding decision could be the step that takes your business to the next level.

About Aneri Shah

Aneri Shah is the Director at Brokers Support Global (BSG), where she leads operations focusing on back-office support for Australian mortgage brokers. With over 4+ years of experience, Aneri specialises in loan processing, mortgage packaging, serviceability calculations, and post-settlement services.