Pre-Approval to Unconditional: A Broker’s Spring File Checklist

Spring is here, and with it comes one of the busiest times of the year for property buyers, sellers, and of course, mortgage brokers. The season brings heightened buyer activity, shorter finance clauses, and lenders rolling out competitive offers. For brokers, it also brings pressure to keep every file moving smoothly from mortgage pre approval to approval without delays or compliance slip-ups.

That’s where a structured file checklist becomes more than just handy, it’s essential. In this blog, we’ll break down the full journey from pre-approval to unconditional approval, share practical steps for brokers, and offer a ready-to-use checklist that helps keep everything on track during spring’s peak property rush.

Why a Spring File Checklist Matters for Brokers

Spring is when the property market comes alive. More listings hit the market, buyers rush to inspections, and competition intensifies.As reported in real estate’s PropTrack Home Price Index (September 2025), national home prices rose 0.5% in September and are 6.2% higher year-on-year, showing strong buyer demand heading into the season. For brokers, that means:

- Higher application volumes – more files to juggle and greater chance of missed steps.

- Shorter timelines – clients are often under pressure to meet tight finance clauses.

- Rising expectations – clients want not just speed but also clear guidance.

- Compliance obligations – ASIC and lenders don’t make exceptions during the busy season.

A well-organised checklist ensures that every client moves from mortgage pre approval process through to unconditional approval smoothly, all while keeping files compliant and audit-ready.

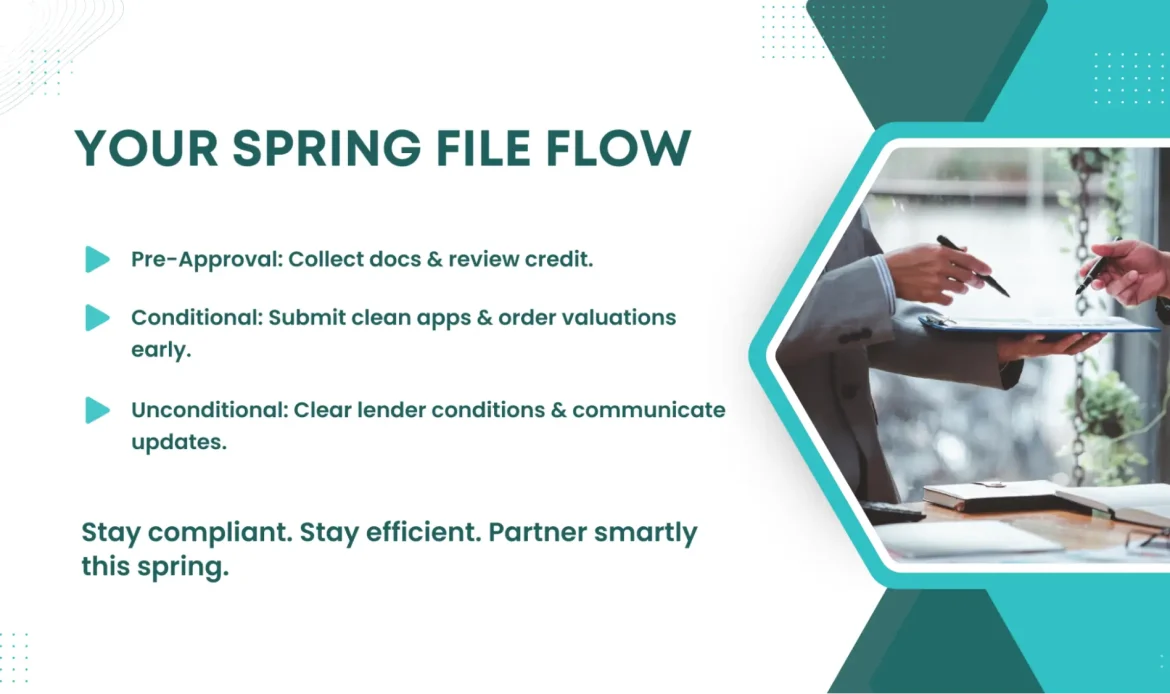

Stage One – Pre-Approval Essentials

Getting the pre-approval stage right sets the tone for the rest of the journey. This is where brokers can either build client confidence or set themselves up for a scramble later.

1. Collecting Documents

Start by gathering the essentials:

- Proof of ID

- Income documents (payslips, tax returns, business financials if self-employed)

- Savings and bank statements

- Details of liabilities, credit cards, and loans

- Living expenses breakdown

Missing or incomplete documents are one of the biggest reasons for delays. A simple mortgage compliance checklist helps ensure nothing slips through the cracks.

2. Reviewing Credit Reports

Pulling a credit report early and addressing any potential issues upfront can save headaches later. Even small errors can hold up a file if not spotted early.

3. Setting Client Expectations

This is also the stage to explain what pre-approval actually means. Many clients mistake it for a guarantee. Make sure they understand the difference:

- A pre approval letter confirms they’re likely eligible to borrow a certain amount, but it’s subject to conditions.

- It’s an indicator of borrowing power, not a guarantee of unconditional approval.

4. Broker’s Tip

Consider creating a “pre-approval pack” for each client with a checklist of required documents, FAQs about the loan pre approval process, and a simple timeline. This adds professionalism and reduces back-and-forth later.

Stage Two – Conditional Approval Readiness

Once pre-approval is in place and your client has found a property, it’s time to push towards conditional approval. This stage is where brokers’ attention to detail makes the biggest difference.

With higher volumes and tighter deadlines, having reliable backend support becomes crucial. Many brokers work with outsourcing mortgage loan processing partners like BSG to streamline documentation, lender communication, and file tracking during busy periods. This ensures consistency and efficiency without pulling focus away from client relationships.

1. Submitting a Clean Application

Ensure the application form mirrors the supporting documents exactly. Common errors, like mismatched income figures or missed liabilities, can lead to unnecessary queries from the lender.

2. Checking Lender Policies

Lenders often run spring campaigns with competitive offers, but their policies may differ. Choosing the right lender based not only on rates but also on service levels and turnaround times is crucial.

3. Ordering Valuations Early

Valuations are one of the most common bottlenecks in spring. Get them ordered as early as possible to avoid delays in moving from conditional to unconditional.

4. Tracking Progress

Set up reminders in your CRM or task management system to follow up with lenders regularly. The goal is to be proactive rather than reactive.

5. Broker’s Tip

Clients love speed. Offering a quick mortgage pre approval experience during this stage not only impresses them but also helps you manage volumes more effectively.

Stage Three – From Conditional to Unconditional

Conditional approval means the lender has looked at the application and is broadly satisfied, but certain conditions still need to be cleared before unconditional approval is granted. This is the critical stage where files can stall if not managed carefully.

1. Clearing Conditions

Common conditions include:

- Updated payslips or bank statements

- Confirmation of insurance

- Satisfactory valuation results

- Proof of deposit transfers

Aim to collect and submit these in one clean batch to the lender to avoid piecemeal back-and-forth.

2. Cross-Checking Contracts

Work closely with solicitors or conveyancers to ensure the contract of sale matches the lender’s requirements. Even small discrepancies can cause unnecessary delays.

3. Keeping Clients Informed

Clients often feel anxious at this stage. Regular updates, even if there’s no change, reassure them that their broker has everything under control.

4. Broker’s Tip

Keep a simple tracker of “conditions outstanding vs conditions cleared” for every file. It’s an easy way to stay organised and spot issues before they escalate.

Spring-Specific File Risks and Considerations

Spring adds extra pressure to the already delicate process of moving from mortgage broker pre approval to unconditional. Here are some risks to watch for:

- High volumes → Lenders often experience slower service levels, so early submissions are key. Recent market coverage by BrokerNews highlighted that buyer demand this spring has been partly fuelled by FOMO, with many rushing to secure loans before further rate or price changes. This surge adds extra pressure on brokers to manage tight timelines without compromising compliance

- Rate changes → Stay updated on lender announcements, as fixed and variable offers can change quickly.

- Shorter finance clauses → Negotiate realistic timelines with clients upfront.

- Compliance pressure → Cutting corners to meet deadlines may lead to compliance breaches later.

Broker Tip: Dedicate 15 minutes each morning to review lender service updates. It’s a small habit that can prevent big surprises.

As mentioned in a Real estate’s report, recent RBA rate decisions have made it tougher for both buyers and brokers, leading to more cautious lending conditions even amid strong spring activity. Staying across lender announcements and rate changes is key to keeping your pipeline moving smoothly.

The Broker’s Spring File Checklist

Here’s a practical table you can use as a ready reference throughout the season:

| Stage | Action Item | Broker Tip / Note |

|---|---|---|

| Pre-Approval | Collect all client docs (ID, income, savings, liabilities, expenses) | Use a mortgage compliance checklist to stay consistent |

| Review credit report | Fix issues early to avoid lender concerns | |

| Issue and explain pre-approval letter | Clarify that it’s not a guarantee | |

| Conditional | Submit clean application (matching docs) | Double-check numbers match |

| Review lender policies and spring offers | Pick lender based on turnaround & client fit | |

| Order valuation early | Avoid spring bottlenecks | |

| Follow up proactively with lender | CRM reminders help stay on track | |

| Unconditional | Collect outstanding docs (insurance, payslips) | Submit in one batch to reduce delays |

| Clear conditions with lender | Keep email confirmation | |

| Cross-check contract of sale | Involve solicitor early | |

| Regular client updates | Builds trust and reduces anxiety | |

| Spring Risks | Monitor daily lender updates | Rate changes are common this season |

| Manage shorter finance clauses | Set client expectations early | |

| Keep compliance files audit-ready | Save all communication logs |

Final Thoughts

Spring is a season of opportunity for buyers, and a season of pressure for brokers. By using a clear, stage-by-stage approach, you can ensure that every file progresses smoothly from mortgage pre-approval to approval, even when volumes are high and deadlines are tight.

A disciplined checklist is more than just a productivity tool; it’s the key to staying compliant, building client trust, and delivering results when the market is moving at full speed.

For brokers, spring doesn’t have to mean stress. With the right process in place, it can be the season where efficiency and professionalism shine the brightest.

If your brokerage is looking to streamline loan processing and stay ahead of spring’s demand, Brokers Support Global helps ensure every file moves from pre-approval to unconditional seamlessly and compliantly.

About Aneri Shah

Aneri Shah is the Director at Brokers Support Global (BSG), where she leads operations focusing on back-office support for Australian mortgage brokers. With over 4+ years of experience, Aneri specialises in loan processing, mortgage packaging, serviceability calculations, and post-settlement services.